SCGD เผยไตรมาส 3 และ 9 เดือน ปี 2568 กำไรเพิ่ม 37% ท่ามกลางความท้าทายเศรษฐกิจ

SCGD เผยไตรมาส 3 และ 9 เดือน ปี 2568

กำไรเพิ่ม 37% ท่ามกลางความท้าทายเศรษฐกิจ

เร่งผลิต-ส่งออกเวียดนามเด่น เตรียมรับดีมานด์ตลาดอาเซียนโต

ดันสินค้า HVA เข้าถึงผู้บริโภคทุกไลฟ์สไตล์ หนุนศักยภาพแข่งขัน

28 ตุลาคม 2568 – SCGD เผยผลประกอบการไตรมาส 3 กำไร 305 ล้านบาท เพิ่มขึ้น 37% โตเทียบไตรมาสก่อน และดีที่สุดตั้งแต่เข้าจดทะเบียนในตลาดหลักทรัพย์ โดยมี PRIME ประเทศเวียดนามเป็นฐานการผลิตส่งออกทั่วอาเซียน เพิ่มประสิทธิภาพการผลิต-บริหารต้นทุน อีกทั้งพัฒนาสินค้า HVA และกลุ่มสินค้าใหม่ในประเทศไทยเข้าถึงผู้บริโภคครอบคลุมทุกไลฟ์สไตล์

%20%E0%B8%AB%E0%B8%A3%E0%B8%B7%E0%B8%AD%20SCG%20Decor%20(SCGD).jpg)

นายนำพล มลิชัย ประธานเจ้าหน้าที่บริหารและกรรมการผู้จัดการใหญ่ บริษัทเอสซีจี เดคคอร์ จำกัด (มหาชน) หรือ SCG Decor (SCGD) ผู้นำในธุรกิจเซรามิก วัสดุตกแต่งพื้นผิวและสุขภัณฑ์ในภูมิภาคอาเซียน กล่าวว่า “ผลประกอบการไตรมาส 3 ปี 2568 EBITDA อยู่ที่ 902 ล้านบาท ดีขึ้นร้อยละ 12 จากไตรมาสก่อน และร้อยละ 18 จากช่วงเดียวกันของปีก่อน และมีกำไรอยู่ที่ 305 ล้านบาท ดีขึ้นร้อยละ 37 จากไตรมาสก่อน และร้อยละ 61 จากช่วงเดียวกันของปีก่อน โดยมี EBITDA on sales และอัตรากำไรสุทธิอยู่ที่ร้อยละ 16 และร้อยละ 5.3 ตามลำดับ ทั้งนี้ หากพิจารณาผลประกอบการที่ไม่รวมผลกระทบของ Non-Recurring บริษัทยังคงมีอัตราความสามารถในการทำกำไรดีที่สุด จากการเดินหน้าตามกลยุทธ์ที่เข้มข้นรวมถึงการเร่งปรับตัวเชิงรุกอย่างต่อเนื่อง ขณะที่ผลประกอบการ 9 เดือน ปี 2568 บริษัทมี EBITDA อยู่ที่ 2,513 ล้านบาทและกำไรอยู่ที่ 744 ล้านบาท

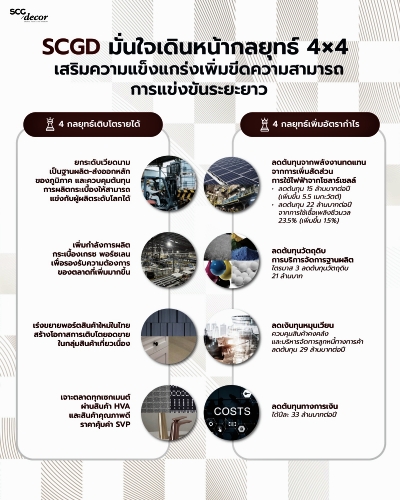

แม้ภาพรวมตลาดวัสดุตกแต่งพื้นผิวและก่อสร้างยังเผชิญความท้าทายจากภาวะเศรษฐกิจและการแข่งขันรุนแรง แต่ SCGD ยังสามารถรักษาความสามารถในการแข่งขันได้อย่างแข็งแกร่ง จากการบริหารจัดการต้นทุนอย่างมีประสิทธิภาพ และการมุ่งพัฒนาสินค้า HVA และกลุ่มสินค้าใหม่ที่สร้างมูลค่าเพิ่มให้กับธุรกิจและตอบโจทย์ความต้องการของผู้บริโภคยุคใหม่ ขณะเดียวกัน ยังเดินหน้าขยายศักยภาพการผลิตในต่างประเทศโดยเฉพาะเวียดนาม ซึ่งเป็นฐานการผลิตและส่งออกหลักของภูมิภาคอาเซียน เพื่อรองรับความต้องการวัสดุก่อสร้างที่ฟื้นตัวขึ้นในประเทศรวมถึงการขยายสู่ตลาดโลกในอนาคต มั่นใจเดินหน้าเสริมความแข็งแกร่งและเพิ่มขีดความสามารถการแข่งขันระยะยาวด้วยกลยุทธ์ 4x4 ดังนี้

1.) ยกระดับ PRIME ประเทศเวียดนามเป็นฐานผลิต-ส่งออกหลักของภูมิภาค เน้นบริหารและควบคุมต้นทุนการผลิตกระเบื้องให้สามารถแข่งกับผู้ผลิตระดับโลกได้ และใช้ความได้เปรียบด้านต้นทุนนี้ขยายตลาดส่งออก ในไตรมาส 3 ส่งออกกระเบื้องทั้งสิ้น 2.2 ล้านตารางเมตร เพิ่มสูงขึ้นร้อยละ 47 เมื่อเทียบกับช่วงเดียวกันของปีก่อน

2.) เพิ่มกำลังการผลิตและดันยอดขายกระเบื้องเกรซ พอร์ซเลน เพื่อตอบรับความต้องการของตลาดที่เพิ่มมากขึ้น โดยเพิ่มกำลังการผลิตกระเบื้องเกรซ พอร์ซเลน ที่ PRIME เพื่อรองรับความต้องการวัสดุตกแต่งพื้นผิวคุณภาพสูงที่เพิ่มขึ้นทั้งในเวียดนามและตลาดส่งออก ในไตรมาส 3 มียอดขายกระเบื้องเกรซพอร์ซเลนจาก PRIME กว่า 3.6 ล้านตารางเมตร จากกระแสของผู้บริโภคที่นิยมวัสดุสวย ทน และดูแลรักษาง่าย พร้อมชูจุดแข็งด้านต้นทุนการผลิตที่แข่งขันได้ในระดับโลก

3.) เร่งขยายพอร์ตกลุ่มสินค้าใหม่ในประเทศไทย เพื่อสร้างโอกาสในการเติบโตยอดขายในกลุ่มสินค้าเกี่ยวเนื่องต่อจากธุรกิจหลัก และสินค้าใหม่ โดยอาศัยศักยภาพในการจัดหาที่แข็งแกร่ง ซึ่งในไตรมาส 3 เติบโตร้อยละ 50 เทียบกับช่วงเดียวกันของปีก่อน

4.) เจาะตลาดเพื่อเพิ่มยอดขายทุกเซกเมนต์ ผ่านสินค้ามูลค่าเพิ่มสูง (HVA) โดยมีสัดส่วนการขายสินค้ากว่า 41% ต่อรายได้จากการขาย เข้าถึงทุกไลฟ์สไตล์ ตอบโจทย์คนรุ่นใหม่ รักสุขภาพ-ใส่ใจสิ่งแวดล้อม ความต้องการของผู้บริโภคที่ต้องการสินค้าที่คุณภาพดี ดีไซน์สวย และฟังก์ชันที่คุ้มค่า เช่น วัสดุตกแต่งพื้นผิว กระเบื้องสุขอนามัย ยับยั้งการเจริญเติบโตของเชื้อไวรัส ผนังดูดซับกลิ่นไม่พึงประสงค์ และผลิตภัณฑ์ “ผนังที่หายใจได้” วัสดุปิดผิวผนังนวัตกรรมจากญี่ปุ่น (Flowel Pure TECH by COTTO) ดูดซับสารระเหยอันตราย และปรับสมดุลความชื้นในอากาศ สินค้ากลุ่มสุขภัณฑ์ สุขภัณฑ์อัตโนมัติ DUACT – TAP & GO ตอบโจทย์ทุกคนในครอบครัว ประหยัดน้ำเพียง 4.5 ลิตร ใช้แบตเตอรี่แทนการเสียบปลั๊ก และก๊อกน้ำรุ่น Xquisia จาก COTTO ดีไซน์หรูฟังก์ชันทันสมัย ซึ่งทั้ง 2 สินค้าคว้ารางวัลออกแบบผลิตภัณฑ์ยอดเยี่ยมระดับสากล รวมถึง สุขภัณฑ์รักษ์โลกใช้สารเคลือบวัสดุธรรมชาติจากเปลือกไข่และเปลือกหอย ที่ช่วยลดการปล่อยก๊าซเรือนกระจก และกระเบื้องที่ลดการปล่อย CO2 ตลอดกระบวนการผลิต

นอกจากนี้ บริษัทยังนำเสนอสินค้าสำหรับกลุ่มตลาดกลางถึงตลาดมวลชนด้วยสินค้าคุณภาพดี และราคาเหมาะสมอีกด้วย

สำหรับ กลยุทธ์เพิ่มความสามารถในการทำกำไร 4 กลยุทธ์ในไตรมาส 3 ปี 2568 ได้แก่ การลดต้นทุนด้านพลังงานผ่านการเพิ่มการใช้เชื้อเพลิงชีวมวลและพลังงานแสงอาทิตย์ โดยมีการเพิ่มสัดส่วนการใช้ไฟฟ้าจากโซลาร์เซลล์ 13.6% เพิ่มขึ้น 5.5 เมกะวัตต์จากไตรมาสก่อน ช่วยลดต้นทุนได้ 22 ล้านบาทต่อปี ขณะที่การใช้เชื้อเพลิงชีวมวล 23.5% เพิ่มขึ้น 1.5% จากไตรมาสก่อน ลดต้นทุนเพิ่มอีก 15 ล้านบาทต่อปี เจรจาการลดต้นทุนวัตถุดิบได้กว่า 21 ล้านบาท รวมถึงการบริหารจัดการฐานผลิตของ SCGD ในองค์รวมเพื่อให้เกิดประสิทธิภาพสูงสุด โดยให้ PRIME เป็นฐานการผลิตและส่งออกสินค้าไปยังตลาดที่เหมาะสม เช่นการส่งออกกระเบื้องจาก PRIMEไปยังตลาดประเทศฟิลิปปินส์ สามารถประหยัดต้นทุนได้ร้อยละ 25 เมื่อเทียบกับต้นทุนกระเบื้องที่ผลิตในประเทศฟิลิปปินส์อีกทั้ง การลดต้นทุนการบริหารจัดการด้วยการปรับลดเงินทุนหมุนเวียน (Working Capital) อย่างต่อเนื่อง ด้วยการควบคุมสินค้าคงคลัง และบริหารจัดการลูกหนี้ทางการค้า ช่วยลดต้นทุนได้ 29 ล้านบาทต่อปี และการลดต้นทุนทางการเงินได้ปีละ 33 ล้านบาทต่อปีจากการทำสัญญากู้ยืมเงินใหม่เพื่อชำระหนี้เงินกู้เดิม รวมถึงการชำระหนี้บางส่วน”

%20%E0%B8%AB%E0%B8%A3%E0%B8%B7%E0%B8%AD%20SCG%20Decor%20(SCGD).jpg)

นายสิทธิชัย สุขกิจประเสริฐ ประธานเจ้าหน้าที่สายงานการเงิน บริษัทเอสซีจี เดคคอร์ จำกัด (มหาชน) หรือ SCG Decor (SCGD) กล่าวว่า “สำหรับใน 9 เดือนแรกของปี 2568 สามารถขยายธุรกิจสุขภัณฑ์ไปยังต่างประเทศ และเพิ่มผู้แทนจำหน่ายเป็น 181 ราย และมียอดขายสุขภัณฑ์ในต่างประเทศ อยู่ที่ 372 ล้านบาท รวมทั้งหลังจากเริ่มจำหน่ายวัสดุตกแต่งพื้นผิว SPC (Stone Plastic Composite) จากโรงงานในประเทศแทนการนำเข้า ทำให้มีความได้เปรียบด้านต้นทุนรวมค่าจัดส่ง ส่งผลให้ปริมาณการขายในช่วง 9 เดือนแรกอยู่ที่ 876,000 ตารางเมตร เพิ่มขึ้นร้อยละ 47 จากช่วงเดียวกันของปีก่อน สำหรับการขยายธุรกิจสินค้าและบริการเกี่ยวเนื่อง เพื่อต่อยอดไปสู่อาเซียนในอนาคต ใน 9 เดือนแรกของปี 2568 มียอดขายกว่า 312 ล้านบาท เพิ่มขึ้นร้อยละ 17 เมื่อเทียบกับช่วงเดียวกันของปีก่อน

บริษัทมีสินทรัพย์รวมทั้งสิ้น 37,064 ล้านบาท และยังคงความแข็งแกร่งทางการเงินด้วยอัตราส่วนหนี้สินสุทธิต่อ EBITDA ที่ 1.3 เท่า ลดลงจากไตรมาสก่อน และอัตราส่วนหนี้สินสุทธิต่อส่วนของผู้ถือหุ้นที่ 0.2 เท่า พร้อมเติบโตในระยะยาว รวมทั้งยังมีการจัดการเงินทุนและการใช้จ่ายอย่างรอบคอบ เน้นให้สอดคล้องกับแผนการเติบโตในอนาคต”

SCGD Reports 37% Profit Growth in Q3 and 9M/2025 Results amid the Challenges

Focus on Vietnam as strategic Production

and Export hub to support Growing ASEAN market

Expand HVA products for all Consumer Lifestyles to enhance Competitive Advantage

October 28, 2025 – SCGD announced third-quarter operating results with net profit of 305 million Baht, representing a 37% increase compared to the previous quarter and marking the best performance since listed in Stock Exchange of Thailand. The Company has positioned PRIME Vietnam as its regional production and export hub across ASEAN while improving production efficiency, managing costs, and developing HVA products and New Growth business in Thailand to respond to consumers across all lifestyles.

Mr. Numpol Malichai, Chief Executive Officer and President of SCG Decor Public Company Limited (SCGD), a leading Decorative Surface, and Bathroom business in ASEAN region, stated that the Company's third-quarter 2025 performance showed EBITDA of 902 million Baht, improving 12% from the previous quarter and 18% from the same period last year. Net profit reached 305 million Baht, up 37% from the previous quarter and 61% from the same period last year, with EBITDA on sales was 16% and Net Profit margin was 5.3%. When excluding non-recurring items, the Company still maintained its best profitability through intensive strategic execution and continuous efficiency improvement initiatives. For 9M 2025, the company achieved EBITDA of 2,513 million Baht and net profit of 744 million Baht.

Despite ongoing challenges of the overall decorative surface and construction materials market due to economic conditions and intense competition, SCGD has maintained strong competitiveness through efficient cost management and focused on developing HVA and New Growth business that create added value for the business while meeting modern consumer demands. Simultaneously, the Company continues expanding production capacity overseas, particularly in Vietnam, which serves as the main production and export base for ASEAN region to accommodate recovering construction materials demand domestically and increasing global market expansion. The Company remains confident in strengthening its position and enhancing long-term competitiveness through its 4x4 strategy as follows:

1. Elevating PRIME Vietnam as the Region's primary Production and Export Base: The Company manage and control production costs against those of world-class players and leverage this cost advantage to expand export markets. In Q3, PRIME exports a total of 2.2 million square meters tile, a 47% increase from the same period last year.

2. Increasing Glazed Porcelain Tile Production Capacity and Sales: To meet growing market demand, the Company expanded glazed porcelain tile production capacity at PRIME to accommodate increasing demand for high-quality decorative surface in both Vietnam and export markets. Q3 sales of glazed porcelain tiles from PRIME exceeded 3.6 million square meters, driven by consumer preferences for beautiful, durable, and easy-to-maintain materials while leveraging globally competitive production costs.

3. Accelerating Expansion of New Growth Product Portfolio in Thailand: This creates growth opportunities for Complementary product and New Growth business, leveraging strong procurement capabilities. In Q3, this segment grew 50% from the same period last year.

4. Penetrating Markets to Increase Sales Across All Segments Through High Value-Added (HVA) Products: HVA products accounted for over 41% of sales revenue, reaching all lifestyles and meeting the needs of health-conscious, environmentally aware younger generations seeking for quality products with attractive designs and valuable function. Decorative Surface products include Hygienic tiles, anti-microbial decorative surface for wall that is breathable and can absorb unpleasant odor (Flowel Pure TECH by COTTO) - an innovative wall surface material from Japan that absorbs harmful volatile substances and balances air humidity. Sanitary ware products include the automatic DUACT-TAP & GO toilet that serves all family members, saves water with only 4.5 liters per flush, uses batteries instead of plugging in; and Xquisia faucet from COTTO with luxurious design and modern functions, both guaranteed by international product design excellence awards. Additionally, eco-friendly sanitary ware uses natural coating materials from eggshells and shells that help reduce greenhouse gas emissions and Tile that reduce CO2 emissions throughout the production process.

The company also offers products for mid- to mass-market segments with good quality at affordable prices.

For another Four profitability enhancement strategies, the Company reduce energy costs through increased usage of biomass fuel and solar power. Solar cell electricity usage increased to 13.6%, up 5.5 megawatts from the previous quarter, reducing costs by 22 million Baht annually. Biomass fuel usage reached 23.5%, up 1.5% from the previous quarter, reducing costs by an additional 15 million Baht annually. The Company negotiated raw material cost reductions of over 21 million Baht and focus on Regional Optimization for example, exporting tiles from PRIME to the Philippines market saves cost at 25% compared to tiles produced in the Philippines. The Company also reduced administrative costs through continuous working capital reduction by controlling inventory and managing account receivables, saving 29 million Baht annually, and reduced financial costs by 33 million Baht annually through refinancing existing loans and partial debt repayment.

Mr. Sitichai Sukkitprasert, Chief Finance Officer of SCG Decor Public Company Limited (SCGD), stated that during the first nine months of 2025, the company successfully expanded its sanitary ware business internationally, increasing distributors to 181 with overseas sanitary ware sales of 372 million Baht. After starting domestic SPC (Stone Plastic Composite) product sales from local factories instead of imports, the Company gained cost advantages including delivery costs, resulting in sales volume of 876,000 square meters during the first nine months, a 47% increase from the same period last year. For the expansion of Complementary businesses in ASEAN, SCGD realized 312 million Baht, up 17% from the same period last year.

The company has total assets of 37,064 million Baht and continues its financial strength with a net debt to EBITDA ratio of 1.3 times, down from the previous quarter, and a net debt to equity ratio of 0.2 times, positioning the company for long-term growth while maintaining prudent capital management and spending aligned with future growth plans.